The intent of The Mint Money Supply Digest is to provide insight via the observation of changes in the trend of our Key Indicators as to the direction of one simple yet critically important trend.

The simple trend is that of the money supply in terms of US dollars. The goal of the monetary stimulus every central bank on the planet has undertaken to some degree or another over the past three to four years has been to simply increase the money supply and hope for the best.

The strategy is a recipe for disaster, as we have explored in depth both here at The Mint and in our eBook series “Why what we use as Money Matters.” The goal of The Mint Money Supply Digest is to keep our readers informed as to the trend of the Money Supply in terms of US dollars in an effort to keep you ahead of the curve when the disasters (for there will be a series of them) occur.

The disasters will come in one of two flavors. The first flavor, which we will call vanilla for the moment, takes the form of the increases in the money supply begin to take hold to the point where inflationary expectations by a majority of the actors in the world economy who use dollars or dollar proxies (currencies and debt instruments which are pegged, directly or indirectly, to the US dollar) in trade become embedded to the point where inflation in consumer prices sparks a level of demand in consumer goods which quickly outstrips supplies of such goods. The vanilla disaster is a mouthful, and it is where the trend is gently heading today.

The second flavor, the disaster which is unlikely in the short term save the appearance of black swan type events, we will call the chocolate variety. The chocolate variety of disaster is simple, it takes the form of an unmitigated collapse in the money supply similar to what the world experienced in 2007 (which most people realized was occurring in 2008). Were this to occur, it is time to get all chips off of the table. Fortunately, our Key Indicators should give us roughly three to four years of advance warning of a full blow chocolate disaster taking place (barring the unpredictable, or black swan event, as it were).

As you can see, while the chocolate disaster is to be feared above all, it will be easier to prepare for given the lead time in the data. The vanilla disaster, which is currently underway to some extent, will be somewhat more difficult to pinpoint in terms of timing but will likely have a lead time of roughly two to three months in which to take action.

Our bias, then, at the outset of The Mint Money Supply Digest, is to be on the lookout for the vanilla disaster while gauging, via the trends in our Key Indicators, just how much chocolate is mixed into the swirl which is the combined disaster that is slowly unfolding in US dollar land.

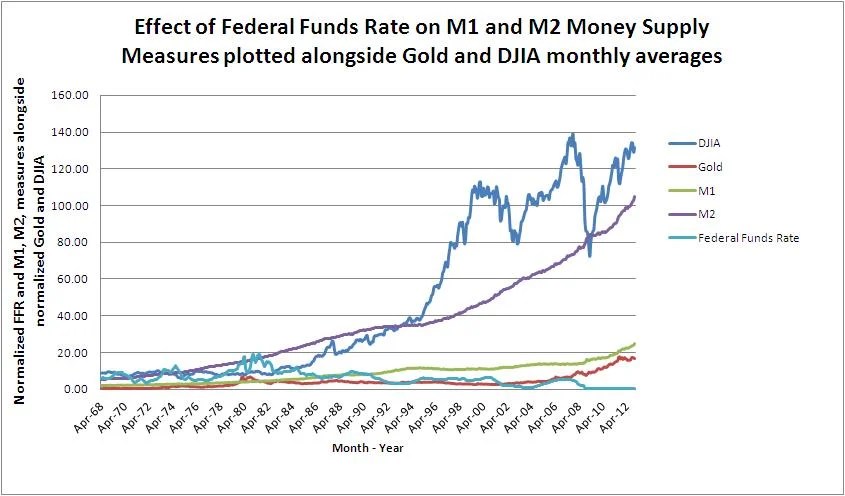

As a logical offshoot of our analysis, we keep an eye on something we call the “Monetary Premium,” which is our term for what most people simply refer to as money. In our worldview, money does not exist in the tangible way that most people assume it does. Rather, the concept of money comes into being when people begin to attach the attributes of money to something which gives that something (usually one of our Key Indicators) a premium above and beyond what normal market conditions and that special “something’s” physical or ethereal composition might otherwise dictate.

This increase in relative value of that special “something” is what we refer to as the Monetary Premium, and it is important, for a big part of making money is accurately identifying not where the monetary premium is, such as the US dollar, but in where it is gravitating towards, such as gold, Bitcoins, or sea shells.