7/14/2014 Portland, Oregon – Pop in your mints…

A great deal has occurred since our last correspondence, most of it bad news for what passes today as monetary policy.

Fellow taxpayers have no doubt noticed that our once faithful correspondence has been less than faithful over the past several months. While explanations amongst chums the likes of which we have become are unnecessary, we offer a brief glimpse as to how The Mint has been spending his precious time as of late.

For starters, we have been frantically reconstructing 2013 and making various systems upgrades on our most recent assignment. Now that the work has been done and passed audit, we are moving through regular compliance reports and are about to begin the second part, (our personal favorite) of our not quite patented one/two accounting and treasury systems overhaul: The treasury overhaul part of the program.

Here we digress into what we consider our unique philosophy on data processing with regards to accounting information systems. If you could care less about such matters, please scroll to the next bolded heading to return to

A mere 11 years ago, we considered ourselves an accountant. We acted like an accountant, worked like an accountant, even smelled like an accountant (if indeed accountants can be said to have a smell about them.

Then we went to Spain, and had nothing short of an epiphany, which is as follows: Real business people could care less about proper accounting, they simply want the accounts collected and the bills paid, a steady stream of cash in the bank, and they want to get real-time financial metrics which will let them both know how their past decisions have fared and, more importantly, allow them to make better decisions about the future.

With this epiphany fresh in our mind, we realized that most accounting systems, while built by programmers to serve the business person, had been hijacked by accountants when they were set up, in most cases rendering the information the business person was to receive subject to seemingly infinite torture by the accountants before it could be presented, at which time the information was neither timely or useful to the business person.

With this realization, we developed our two-step approach to assisting business people in reclaiming their accounting data. The first step involves ensuring that the accounting system they are using is both adequate (it may come as a shock that many companies pay too much for systems that are no longer a good fit for them) and set up to capture and report the business’s financial data in a way that facilitates high level decision-making.

The second step involves addressing the issue of the timeliness of the data. We realized that in a great majority of transactions, the bank received the data before the accounting department did, and much valuable time and effort was wasted by waiting for the accounting department to input data into the accounting system, much of which was provided by the bank rather than internal sources, and then reconciling the system to the bank statement. The entire process was backwards, so we decided to perform data processing directly in the banks’ treasury management systems, where the transactions are initiated, approved, and executed, and have the bank data be easily uploaded into the accounting system, where it can be matched with vendor and client data and properly classified.

There you have it, it is much easier said than done, but once our program is complete, most companies we engage can get by with half of the accounting/fiscal personnel they had before, get their data in a timely and coherent manner, and usually end up saving money on their systems to boot.

In any event, between earning our daily bread in the above manner, watching the World Cup, and editing a taxonomic paper on Central American land crabs (which can be seen here: http://biodiversitydatajournal.com/articles.php?id=1161), we have been following the disintegration of the debt based currency system from a comfortable distance. Our observations on the most recent ruptures follow:

The No bid Repo: It’s not your father’s overnight funding market

In the late 1980’s, the Federal Reserve had just begun what would be a series of automatic bailouts to the larger financial system. After Black Tuesday in 1987, it became clear to most sober observers that the Fed would do everything in its power, which at the time was limited to rigging short-term interest rates, to ensure that financial markets remained liquid at all costs.

Perhaps not coincidentally, in the late 1980’s, Oldsmobile ran a series of commercials with the tagline, “it’s not your father’s Oldsmobile,” which seemed to be a vain attempt to minimize the “Old” and emphasize the “mobile” part of its name. In case you don’t remember how exhilarating it was, videoarcheology.com brings it to life for us once again:

What did the strategy of the Fed and the strategy of Oldsmobile have in common? They both assumed that demand for their product, no matter how unappealing it was, would be infinite. Oldsmobile gave up the ghost in 2004, maybe people did want their father’s Oldsmobile after all.

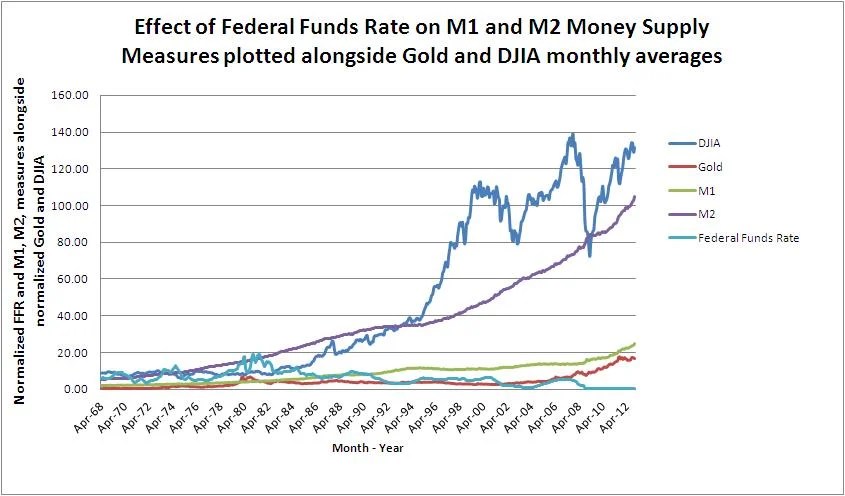

The Fed is still hard at work, but their product, the debt-based currency used by most financial institutions in the United States and indeed throughout the world, is going the way of the Oldsmobile.

The Federal Reserve got by for nearly 95 years by monopolizing the ability to provide something for nothing, something that appealed to governments, companies, and consumers alike. They substituted debt for money, and in the process opened up a world of possibilities never before fathomed.

The plan went well, people began to circulate the debt in place of money, with those closest to the Fed paying the least and those furthest way paying more, and people toiled day in and day out to move further up the food chain.

Sure, using debt as money left the occasional sinkhole in the economy, on those rare occasions when more debts were being cancelled than issued, but the Fed simply lowered interest rates to provide adequate incentive for people to demand more debt, lowering the perceived price of getting something for nothing.

Now, circa 2014, the Fed has lowered interest rates to zero and has taken the extra step of creating even more debt of its own to circulate. While things should be going gangbusters at the Fed factory, we open the pages of the financial news to find that:

a) The Fed can no longer control the interest rate mechanism as it did before and;

b) The Repo market, which funds $1.6 trillion in short-term loans every business day, is going no bid on an increasingly regular basis thanks to the 2010 Dodd-Frank Act, which was supposed to fix these sort of problems.

{Editor’s Note: For a primer on the Repo Market, read this paper by the NY Fed: Key Mechanics of the U.S. Tri-Party Repo Market, we dare you}

The Federal Reserve’s debt based monetary system has reached its theoretical limit. While the ECB has toyed with the idea of negative interest rates, the US market, specifically US Treasuries which are sucked into the Repo Market nightly, is rendering negative rates on its own, and the Fed is powerless to stop it.

In layman’s terms, the game has flipped on the Fed, and now people and companies are essentially saying “lend me $100 today, and I’ll pay you back $97 in a year and we are square.” Crazy as it may sound, this is the reality on the fringe of the credit markets, and it is the price of continuing to deal in a debt-based currency that is passed its prime.

Let’s face it, Oldsmobile wasn’t cool in 1988. They had tinkered with it to such a degree that it would never again be your father’s Oldsmobile, and that was not a good thing. In the same way, between QE, Operation Twist, and near zero short-term rate targeting, Ben Bernanke has so severely mangled the Fed’s balance sheet with his tinkering that maintaining the integrity of the US dollar and US Treasuries as any sort of measure of reliable benchmark is all but impossible.

Now, the engine of the Fed’s debt based currency is beginning to lose speed via negative nominal rates, and Janet Yellen is looking into the toolbox, only to realize that Ben left most of the tools rigged in the engine of the Fed’s Balance sheet, and that moving any one of them will cause a catastrophic failure of the currency. Not to mention that long-awaited, highly inflationary wage – price spiral is about to kick in.

Academic economists will one day struggle to explain what is happening now, while inflation rises, interest rates continue to dip further, going negative at the top of the financial food chain, and the Fed is left with nothing but rhetoric with which to attempt to execute monetary policy. This is likely to get ugly and, if possible, defy the laws of finance and perhaps even mathematics before the game is up.

Stay tuned and Trust Jesus.

Stay Fresh!

Email: davidminteconomics@gmail.com

Key Indicators for July 14, 2014

Copper Price per Lb: $3.25

Oil Price per Barrel: $100.51

Corn Price per Bushel: $3.78

10 Yr US Treasury Bond: 2.52%

Bitcoin price in US: $618.00

FED Target Rate: 0.09%

Gold Price Per Ounce: $1,339

MINT Perceived Target Rate*: 0.25%

Unemployment Rate: 6.1%

Inflation Rate (CPI): 0.4%

Dow Jones Industrial Average: 16,944

M1 Monetary Base: $2,961,000,000,000

M2 Monetary Base: $11,284,500,000,000

You must be logged in to post a comment.