9/11/2015 Portland, Oregon – Pop in your mints…

September 11th has become a day of remembrance in what was formerly the land of the free. The horrific spectacle of the events that unfolded in New York and Washington that infamous day will be forever etched in the memory of our generation. While we did not realize it at the time, it was the day that the United States lost a great deal of freedoms.

The external restrictions that have been imposed on society post 9/11 are well documented. The passage of the Patriot Act has given the government carte blanche when it comes to surveillance and disregard for due process. While these practices have always been employed to some degree, the Patriot Act in a sense legitimized them.

Perhaps more devastating, however, has been the mental shift that 9/11 caused in the thought of US Citizens. Pre 9/11/2001, the US was a place where truly anything was possible, it was the Land of the Free, the sky was the limit. Humankind had just “survived” the Y2K non-catastrophic event and credit flowed freely.

More importantly, though, our minds were free.

Naturally, we can only speak of our own experience, but we would be willing to bet that many who lived these events would agree. Pre 9/11, the United States was a completely different country.

Ironically, 9/11/2001 was the day after we had been laid off from our first job. We had cornered ourselves in Internal Audit, which for the uninitiated, is the first department to get the axe when cost cutting measures are employed. Really, who wants to pay people to tell them what they are doing wrong all day unless they can justify the expense?

We received the memo and our final check on the 10th. On the 11th, we woke up to the first day of freedom that we could recall, turned on Good Morning America, and watched the events unfold. At that point they were speculating that the first tower was some sort of small aircraft accident. A caller from New Jersey was on and said, with a grave seriousness in his voice, that it was not a small aircraft, but a commercial airliner. Then, on live television, the second airplane hit the second tower. We are embedding a YouTube video of this moment for those who did not see it. Please be advised that it is indeed disturbing and skip it if you do not want to be shocked:

It was at that point that we knew something bigger than ourselves was occurring, and God had set us there to PAY ATTENTION TO WHAT WAS GOING ON! We were new to Christianity, true Christianity, and had begun to truly commune with God over the past several months. To those who have not had similar conversations with the creator, this will sound strange, but God does speak quite clearly to those who are paying attention.

Anyway, God said, “It’s time.”

This has set our life on a completely different course, one that you, fellow taxpayer, are now a part of.

Ah yes, we were going to explain why money does not exist, at least not in the sense that most understand it.

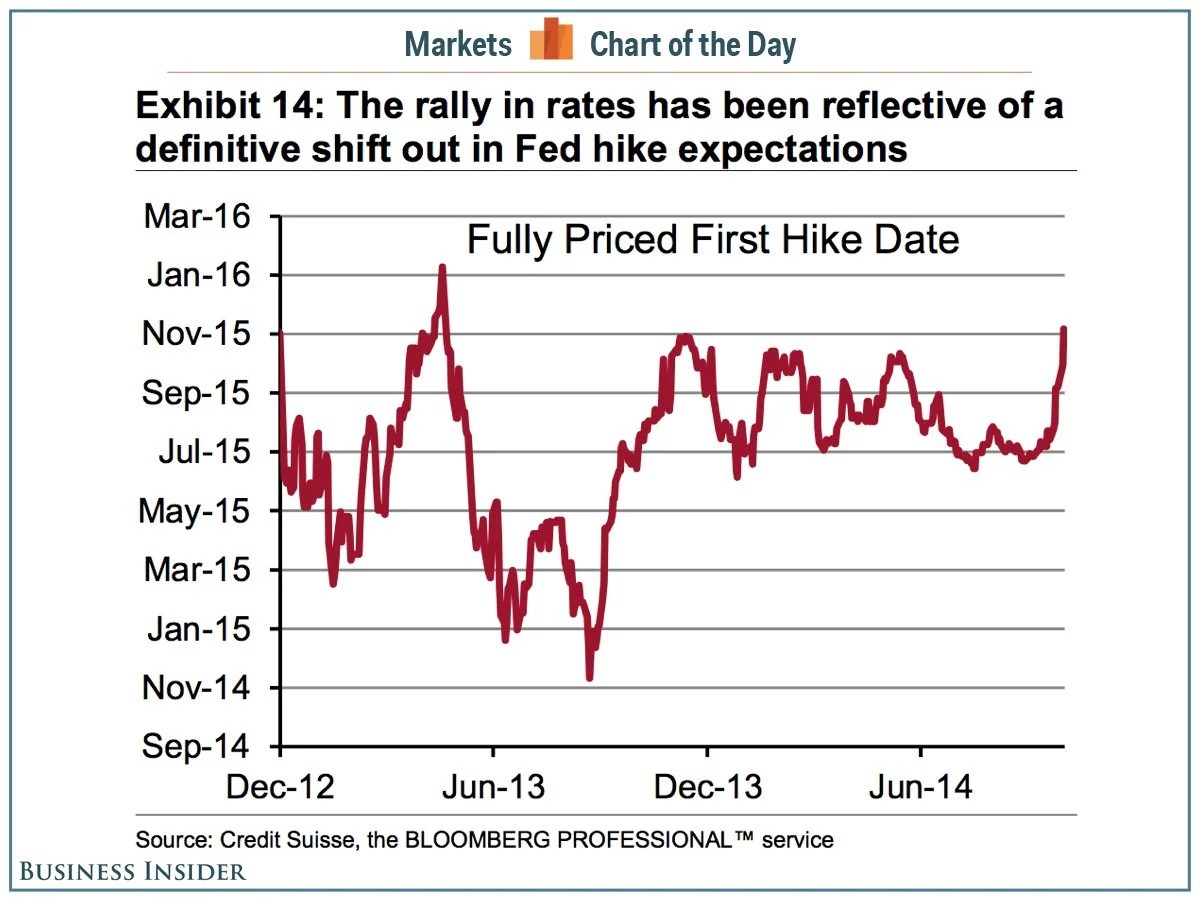

The Federal Reserve is set to meet in September. There is an expectation that they will raise interest rates. However, there is also a sense that the economy is somehow still in a funk. What is the Fed to do?

We postulated earlier this year that the Fed would sooner raise interest rates than end its QE money printing programs. We were wrong, QE ended before rates increased. However, we hold out the spectre that, eventually, perhaps this month, the Fed will need to increase its target rate. When it does, it will cause big problems for large banks. Banks will need a buyer for the masses of Treasuries they have to hold as a result of Dodd-Frank. The Fed will buy them at cost (not market, as their market value will be dropping), effectively reinstating their QE program.

They will raise rates on the short end and work to maintain lower than natural long rates. Anything else would spell disaster for the economy.

Why can the Fed employ QE (electronic money printing) in the first place? Because money does not exist. What we use as money is really credit. Credit and Money are opposite elements in the realm of economics. They should cancel each other out.

Now that Money is credit, the productive activities of humankind are aligning themselves in direct conflict with the needs of the natural world. And the chasing of non-existent money is causing humankind to strip mine the earth.

Will we learn in time?

Stay tuned and Trust Jesus.

Stay Fresh!

Email: davidminteconomics@gmail.com

Key Indicators for September 11, 2015

Copper Price per Lb: $2.43

Oil Price per Barrel: $44.79

Corn Price per Bushel: $3.62

10 Yr US Treasury Bond: 2.19%

Bitcoin price in US: $240.28

FED Target Rate: 0.14%

Gold Price Per Ounce: $1,106

MINT Perceived Target Rate*: 0.25%

Unemployment Rate: 5.1%

Inflation Rate (CPI): 0.1%

Dow Jones Industrial Average: 16,330

M1 Monetary Base: $3,132,300,000,000

You must be logged in to post a comment.