As we begin the month of February, it would appear that the US Economy has suffered from a couple of data shocks, which, taken at face value, would call into question the validity of the current rally in nearly every asset class (save bonds) and give rise to fears of the US slipping into another Recession or worse.

First, the Gross Domestic Product read came in at a negative 0.1% for the fourth quarter. The GDP is mostly a bogus data point in an economy with a debt based currency. At this point, the negative data, like most data that will appear this year, will give the Federal Reserve the statistical cover they need to continue QE and decimate the dollar.

The Unemployment rate, which inched up slightly, falls into the same category. Given the paradigm shift that the US workforce is undergoing as the internet makes geography a non issue for anyone who works from a computer, and the demographic shift as the Baby Boomers ease into retirement make it hard to say what would constitute an appropriate amount of Unemployment at this time.

Full employment has always been a slippery concept, and at this point, the BLS statistics can be counted on to err on the side of covering the inflationary consequences of QE as well.

What has not changed is that people, when given the chance, will tend to spend more money than they have. This tendency is again being allowed to manifest itself as credit restrictions are easing in the US and soon, even your cat will begin to receive credit card offers as they did in the good old days of 2005.

The Federal Reserve and every Central Bank on the planet have stuffed every orifice of the financial system with cash, so much so that they must lend gobs of it out to remain solvent. The consumers are taking the bait, and the wave of inflation is now rolling through stocks and commodities. It will not stop until QE stops.

And given the propaganda that passed as economic data prints this past week, QE will be with us for quite some time. Plan and invest accordingly.

With Japan’s recent aggressive devaluation of the Yen, the financial news has again taken up the phrase “currency war” to describe any lack of coordination in the steady devaluation of fiat currencies across the globe.

In a recent piece over at the Financial Times, Niall Ferguson identifies the Bank of England as the current winner in the stealth currency war that is currently being waged. While the Bank of England may be the winner, the losers are not other nations, as the term war would suggest, but rather the savings of those who are unfortunate to count bank accounts or debt instruments denominated in national currencies among their assets.

Who, then, are the winners in what we have dubbed the currency war to end all currency wars? In a simplified sense, those who hold the Dow Jones Industrial stock index (not the individual stocks, which are, in the final analysis, a crap shoot) and those who own gold.

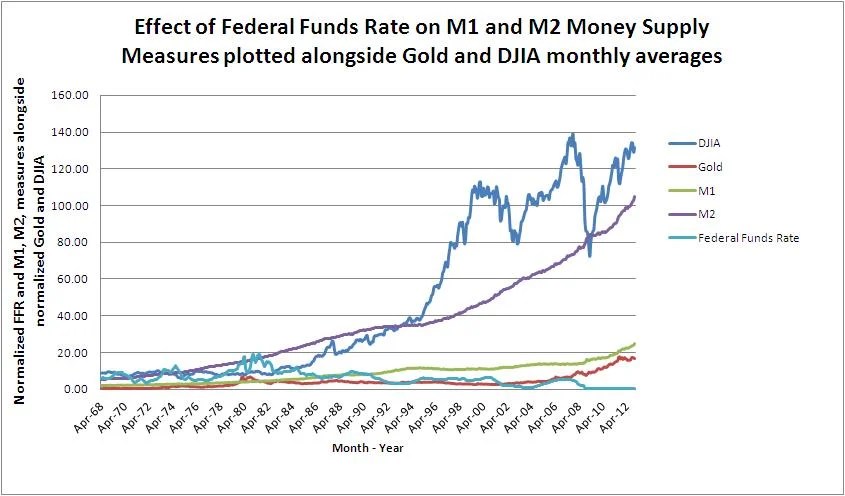

In an attempt to illustrate this point while at the same time saving 1,000 words, should the old adage hold true, we have created the following graph, which plots a normalization (which brings the sheer magnitude of the numbers down to a workable scale) of the M1 and M2 monetary measures against both the Dow Jones Industrial Average and gold prices, all averaged on a monthly basis since April of 1968.

Graph of normalized DJIA and Gold assets classes vs. M1, M2, and Federal Funds Rate measures

Those with a keen eye will notice that the only data point that has been on a downward trend since the US Dollar was officially released from the shackles of the gold standard on August 15, 1971 has been the Federal Funds Rate, which in theory should have an inverse relationship with all of the other data points.

We will leave you with three observations from our graphic exercise:

1. The most volatile of the two asset data sets has been that of the Dow Jones Industrial Average. However, despite its volatility, its overall trend tends to follow that of the M2, or expanded, money supply measure.

2. The more stable of the two asset data sets has been gold, which has generally lagged growth in the M1, or base money supply to which it was tied to pre 1971. Beginning in the year 2000, gold again began to follow the M1 trend.

3. The light blue line, which tracks the Federal Funds Rate, has been on a downtrend. The upticks in the Federal Funds Rate, in theory, should have lead to downward ticks in the M1 and M2 As you can see from the graph, this is not the case.

The conclusion of this brief analysis is the following: Holding Stock Indices such as the Dow Jones should give some measure of protection against inflation over the long term, perhaps even superior to gold. However, since 2000, gold has held steady as an inflation hedge and generally will have less liquidity risk than stocks.

Finally, and perhaps most importantly, is that upwards changes in the Federal Funds rate, even those as dramatic as were experienced during the Volcker years, have little or no effect on the near term trajectory of the M1 and M2 monetary measures and have never caused these monetary measures to trend downwards, ever. At most, these movements may serve to temporarily arrest the upwards slope of the growth of the M1 and M2 monetary measures.

What does it mean? While the Federal Funds Rate may serve to weakly toggle the rise in the M1 and M2 measures, the Quantitative easing programs, which began in 2008 and are now a permanent piece of monetary policy, have had a much greater direct impact on both the monetary measures and the asset classes which have been included above.

Given the current state of affairs, the QE program must be watched closely as it will have an outsized immediate impact on asset prices.

In the long run, it is clear that the Federal Reserve has set monetary policy on autopilot and programmed a course straight through the stratosphere and into the far reaches of outer space. There is no plan for the US Dollar to return to earth. The M1 and M2 monetary measures will not come down, no matter what happens to QE and the Federal Funds Rate.

It is time to organize investments in the real world accordingly.

Last week, we made a vague promise to provide data to back a claim that the US Debt at the FED had already been largely cancelled via the various quantitative easing (QE) operations that have been realized over the past several years. This fact makes any talk of solving the moronic “Fiscal Cliff” via extreme methods such as minting platinum coins with $1 Trillion face value unnecessary.

In an attempt to illustrate what amounts to an effective forgiveness of a portion of the US National Debt by the Federal Reserve, we offer the following graph, which plots the both the official US National debt as well as the official US National debt net of the Federal Reserve’s holdings as a percentage of GDP.

As you can see, the real US National debt to GDP is closer to 94% rather than the projected 105% which the official US National debt figures would suggest. The Federal Reserve, at last count, holds roughly $1.6 Trillion of US Treasury debt. While this debt is still theoretically on the books, it can essentially be removed from consideration when arguing about the need to solve the debt problem, vis-a-vis the moronic Fiscal Cliff debacle that is playing out in Washington.

94% is an alarming level, but according to our projections, the current US Government current account deficit cycle is about to end as the waves of new currency released into the global economy by the Federal Reserve and other central banks begins to run through the coffers of the US Government.

Despite the desperate proclamations by Congress that it will be difficult to solve their (yes, this is their problem) impasse, indicators such as an EFT that tracks the Defense industry, XAR, which would theoretically be the hardest hit were the US to fail to address portions of the Fiscal cliff such as suspending the sequestered spending cuts agreed upon as a result of the infamous Debt ceiling debacle, are not showing any signs of trouble.

In other words, the financial markets are assuming that the US Congress and Executive, when push comes to shove, will wind up and kick the can a mile down the road, as they did when the debt ceiling was bearing down on them.

According to our projections, there is no debate, the Fiscal Cliff does not even exist, rather, it is a figment of the collective imagination.

We do not believe in money, at least not in the form of money that is currently used in America today, and it appears that the US Congress is beginning to come around to our point of view. If the Federal Reserve will simply finance deficits ad infinitum, why even bother with the Fiscal Cliff charade? We are still working to answer that question, and leave it for you, fellow taxpayer, to ponder along with us.

The real question, the one which we wrestle with every day here at The Mint, is when will the faith in the Federal Reserve be destroyed? With the advent of the various QEs beginning in 2008, the Federal Reserve system effectively collapsed. The creation of credit was no longer self sustaining in the economy. The FED has been living on borrowed time.

As December 21 approaches and those who have misinterpreted the Mayan calendar wonder if December 22nd will come, we look forward to the 22nd of December, when the Federal Reserve’s charter is rumored to expire, and YouTube’s “Man of Truth” famously prophesied that the Federal Reserve would go bankrupt. Technically, he said “December 2012”, but, after 99 years, why split hairs?

Chances are that the world will wake up on December 22nd and carry on. However, if you see the words “Force Majeure” in the financial headlines, get ready to calculate prices in a new currency for 2013. For the US may swerve to avoid the Fiscal Cliff, but sooner or later it will drop off the currency cliff.

That is when things will get very interesting indeed.

There is much confusion amongst economists regarding the effects of the various programs which are currently being run by the largest of the Western Central Banking cartels known as Quantitative easing, better known by its keystroke saving acronym, QE.

For the uninitiated, QE involves the Central Bank issuing currency in exchange for government debt and all other manner of otherwise worthless financial assets provided to it by the banking class. In the best of cases, it provides liquidity for what would be a temporary hiccup in an otherwise healthy economy. In the worst of cases, which most who have taken a sober look at the financial industry would agree we are in, it serves as a backstop for financial asset prices, placing an artificial floor under the price of what passes as collateral in the financial system.

In any case, the Central Bank agrees to swap the wine of its currency for the sewage on bank balance sheets. As anyone who has put this theory to the test will tell you, if you add a teaspoon of wine to barrel full of sewage, you get sewage, while if you add a teaspoon of sewage to a barrel full of wine, you get…sewage.

QE – Sewage in disguise

Following this analogy, the existence of QE means that the currency of all of the Western world is now sewage.

While the pure, hard money Austrian school analyst sees it as a prelude to a hyperinflationary event, the Keynesian sees it as a necessary evil. At this point, there is no real argument that QE, by definition, is inflationary. However, the perverted feedback loop between the Central banks’ issuance of currency, the Governments’ issuance of debt, and the banking sector serving as an increasingly weak middleman, has managed to keep a large portion of the freshly created currency parked in either the Treasury or at the Central Bank in the form of excess bank reserves.

As the logic of the Central Bank goes, once the storm blows over, the stars will align and all of the sewage will turn back into wine. The currency created as a part of QE will simply disappear, as it never really left the FED anyway.

Simple logic, right? You can almost cut the naivety with a knife. The fact is that the freshly minted currency is here to stay. As long as the Governments, Central banks, and banking cartel exist in their present form, none of them can afford for even a cent of the sewage they have created to disappear. It is there for the long haul. All the average man or woman can hope for is that the sewage doesn’t spill off of their balance sheets or work its way to the water supply of the real economy.

All of this is old hat to fiat currency hounds and bond vigilantes. The dangerous new twist which is just now in its infancy is the application of quantum theory to the mix.

Here, we must turn to the razor sharp intellect of Mr. Walayat, whose analysis over at The Market Oracle is on the cutting edge and generally spot on.

Walayat, along with Lee Adler of the Wall Street Examiner, are amongst the handful of analysts with a true understanding of the banking system and the motives and logical consequences of the actions of the Central banking cartel.

As the currency event in Iran unfolds, those of us in the “secure” West would do well to read up on what awaits as the Western Central banks throw their inflationary machines into overdrive, what Walayat refers to as “The Quantum of Quantitative Easing, or the keystroke saver: QQE.”

The operation of QQE is simple and predictable, yet unnecessarily mind-boggling.

As in a standard QE operation, it begins with the Government issuing debt which is purchased by members of the banking cartel in exchange for currency, which it then spends on any number of pet projects. The Central Bank then buys the Government debt from the banks and receives the interest which is paid by the Government. The Banks park the currency they have received from the Central Bank at the Central Bank and earn interest on it.

QQE ensues when the Central Bank then returns to the Government the difference between the interest paid by the Government on its own debt and the interest paid out to the Banks to keep them afloat. As the Central Bank will never take a nominal loss on their debt holdings, and the Government will never default as long as QE remains in place, The Government is not borrowing at the implied interest rate that it auctions its debt at, rather, it is effectively borrowing at the rate that the banks earn on their reserves deposited at the Central bank, less the cost of the Central Bank’s operations!

Is your head spinning yet? Stay with us, it gets better. The longer that the policy of QE continues (and it will continue until the currencies of the world blow up, as the Iranian Rial is in the process of doing,) the Government is effectively swapping out its old debt, issued 30 years ago at anywhere between 11 and 14%, for new debt at an effective rate of 0.25%! Those interest savings on the rollover are the rocket fuel of QQE. They are what will allow the Governments to both ramp up spending and reduce the relative size of their balance sheet.

By the way, those “savings” come at the expense of every person and organization which holds the currency as a savings vehicle.

In order to gain a fuller understanding of just what is going on, read the articles linked in the above paragraphs at your leisure. They will help to make sense of what is occurring as we begin to see the paradox of increased government spending and reduced or stable levels of national debt.

Oh yes, and double digit real inflation rates, despite the irrelevant claims of the BLS propaganda machine. Plan accordingly, this is not a drill.

We search for answers, yet the questions are trumping them right now. This phenomenon is inherent to human existence. People are always chasing after knowledge. In the Bible, the book of Daniel speaks of our times when the Angel tells Daniel in his vision:

“But you, O Daniel, shut up the words, and seal the book, even to the time of the end: many shall run to and fro, and knowledge shall be increased.”

A little bit of knowledge sparks a thirst for more knowledge, which, once quenched, sparks an even greater thirst for knowledge. Like Carmex, which soothes one’s chapped lips for a time only to dry them out again, which appears to create a perpetual “need” for to the product, knowledge provides answers and understanding which lead the enquirer to even more questions, and the cycle repeats itself.

The phenomenon expresses itself in markets in the form of a search for a “final price”. In a free, unfettered marketplace, this price, in money terms, represents all that is known about the value of the good that is being exchanged for money at that point in time. However, this “final price” is in and of itself a new data point to be considered, as is the exchange of goods which it represents. This changing data necessarily creates a new “final price” which, by definition, takes into account all factors know about the value of the good and so on.

Ever since we decided to eat the fruit of the tree of the knowledge of good and evil, the chase for knowledge has continued and will continue until Jesusreturns.

But what does this have to do with the US Dollar, let alone Beer?

We are glad you asked as we were getting a bit side-tracked. Our personal search for knowledge has brought us to the most recent of the endless questions that need to be answered:

When will Central Bank Currency Regimes and Sovereign Governments admit they are bankrupt and be allowed to default?

This is an URGENT and very important question as the entire financial world cannot progress until this question has been answered.

To be clear, most western governments and their Central Bank run currency regimes are now technically in default. They have been ever since they began to “solve” liquidity problems via money printing or “Quantitative Easing” (QE for short).

The acts of Quantitative Easing, which have been embarked upon by the US, Euro, and Japanese Central Banks is only necessary when the faith based currency regime in question has failed. The necessity to print money which is not demanded by the market nor provided at market prices provides concrete proof that people are no longer willing to further enslave themselves by incurring additional debt.

As we have explained in this space before, debt is the lifeblood of the currency regime. In these mindless confiscatory monetary systems where the only way to create money is to coax someone else into incurring debt, shrinking debt is the equivalent of someone pushing the currency regime’s self destruct button.

But instead of recognizing this fact for what it was, a failure of the system, much of western civilization continues in willful denial. Soon, however, everyone will be rushing for the exits.

But we promised you a beer, fellow taxpayer, so crack yourself a cold one (on your own dime, of course, this is, after all, a free newsletter) and see if you tell us what the Federal Reserve Notes that we currently use as money and Schlitz Beer have in common?

What do Schlitz and the Federal Reserve Note have in Common?

Need a hint? Think quality, or lack thereof.

Give up? Here are the answers, as always, we invite inquiring fellow taxpayers to add to this list by commenting below.

First, both Federal Reserve Notes and Schlitz were once the gold standards of their product class (currency and beer, respectively). Federal Reserve Notes took the place of US Dollars in 1913 and maintained the US Dollar’s tradition of quality and enjoyed increased market share until finally overtaking the British Pound Sterling as the world’s currency of choice. In the beer industry, Schlitz rose to overtake rival Pabst as the most popular beer in the world in 1902.

In the 1970s, the Schlitz brewing process was changed to make use of high temperature fermentation in order to further speed production. This change and subsequent changes in the formula had disastrous results which came to a head in 1982. On the US Dollar front, then President Richard Nixon began to tinker with the US Dollar formula in the 70s, namely making the US Dollar no longer convertible into gold. This watering down of the dollar supply had disastrous effects which also came to a head in the early 1980’s.

Both Schlitz and the US Dollar then continued to generally decline in status for close to 30 years.

In 2008, however, the old Schlitz formula was discovered and has been revived by Stroh’s Brewing Company to give new life to an old beer that everyone had left for dead.

Circa 2011, the US Dollar is still yearning to return to the “gold convertibility” formula that made it so insanely popular for the first half of the twentieth century.

*See MINT Perceived Economic Effect Rate Chart at bottom of blog. This rate is the FED Target rate with a 39 month lag, representing the time it takes for the FED Target rate changes to affect the real economy. This is a 39 months head start that the FED member banks have on the rest of us on using the new money that is created.

You must be logged in to post a comment.