3/29/2014 Portland, Oregon – Pop in your mints…

“…Sanballat and Geshem sent to me, saying, ‘Come, let us meet together in the villages in the plain of Ono.’ But they intended to harm me.

I sent messengers to them, saying, ‘I am doing a great work, so that I can’t come down. Why should the work cease, while I leave it, and come down to you?’ They send to me four times like this; and I answered them the same way…”

– Nehemiah 6:3

Nearly 30 days and nights have passed since our last correspondence, fellow taxpayer, and we, like Nehemiah, have only one excuse:

We are doing a great work.

Nehemiah’s great work, referred to above, was to rebuild Jerusalem, the Holy City. He found that, though he had been given authority to perform the work, on the ground, he often encountered hostility and detriments to the work that came from quarters where he had reason to expect help or, at a minimum, indifference.

Our great work at the moment, fellow taxpayer, is to concurrently rebuild a Fiscal department and restore an accounting record that has fallen into disrepair, all while undergoing an annual audit and responding to the day-to-day tasks and myriad of reporting requests which come with the territory of modern financial management.

{Editor’s Note: While it is a subject for another day, we must comment on the tool of the trade that is being employed in the great work, the Yardi Voyager accounting software. We last touched Yardi over 10 years ago and, while the software retains many of its origins, the current version is a beast in terms of cloud processing. We reckon that, given the correct tactician at the helm (which we humbly consider ourselves to be), accounting records in Yardi can be administered by considerably fewer finance staff than many competitors.}

For the moment, we face no hostility and, generally speaking, the finance profession is free from mortal danger. However, there is great interest in the work as there are ultimately a great number of interested parties, and we find that, like Nehemiah, we are often called to the ‘villages in the plain of Ono’ for other matters.

There are risks in undertaking any great work, and there is also great exhilaration in making progress and ultimately, after facing all of the difficulties and suffering through the doubts of naysayers, doing the impossible.

Janet Yellen’s Great Work

Janet Yellen came onto the job as the Federal Reserve’s first Chairwoman on February 3, 2014, just 10 days after we began our great work. Unlike ourselves, Yellen has had the benefit of watching her predecessor hone his craft as Vice Chairman for four years and has enjoyed the benefits of the revolving door between government and academia since the early ’80s.

In other words, Yellen has no real world experience, which is a prerequisite to serve in any high-ranking office in America, circa 2014.

According to her dossier, it counts among her previous great works a study dealing with East Germany’s integration into the German economy upon the reunification of the country. {Editor’s Note: For those to young or indifferent to recall such matters, the East German integration was a major windfall for West Germany at the time, who then (1990) was jockeying for position in what was to be the European Union. The reunification caused 16 million more Germans to appear overnight, giving the unified Germany a considerable voice in the negotiations.} Beyond this, Yellen is given credit for a form of clairvoyance regarding the financial crisis in 2007, apparently seeing something amiss from her post as the President of the San Francisco Fed (she must have seen Jim Cramer’s rant in July).

Janet Yellen now has a new great work to undertake as Chairwoman of the Federal Reserve. While she was likely performing many of Bernanke’s tasks from at least October of last year when President Obama nominated her as Bernanke’s successor, one task that could not be delegated was that of the press conference.

As such, Yellen took the stage on March 19th, 2013 and dutifully attempted to explain the rationale for the decisions of the Federal Reserve’s FOMC regarding short-term interest rates and its Quantitative Easing programs.

The press conferences, which began under Ben Bernanke, were meant to clear up any confusion, which may have been read into the numbers and written statements provided by the FOMC which had until then served as the primary window for the outside world into the machinations of the committee which decides how much credit will be conjured out of thin air.

For some reason, perhaps the novelty, the press conferences have taken on a life of their own. The reason for this is that, while the FOMC may have deliberated and arrived at a consensus regarding their curious task, the person who gives the press conference ultimately has the last word and, though the event is meant to be carefully scripted, it cannot help but introduce an element of uncertainty into a process (the conjuring of credit out of thin air) which already defies the laws of economics and indeed works in direct opposition to nature herself.

At minute 20, which we have clipped below, Jon Hilsenrath of Wall Street Journal calls out the fact that there is an upward drift in a dot plot reflecting expectations for short-term interest rates of the individuals on the committee, and how one should reconcile that with the guidance given in the FOMC statement.

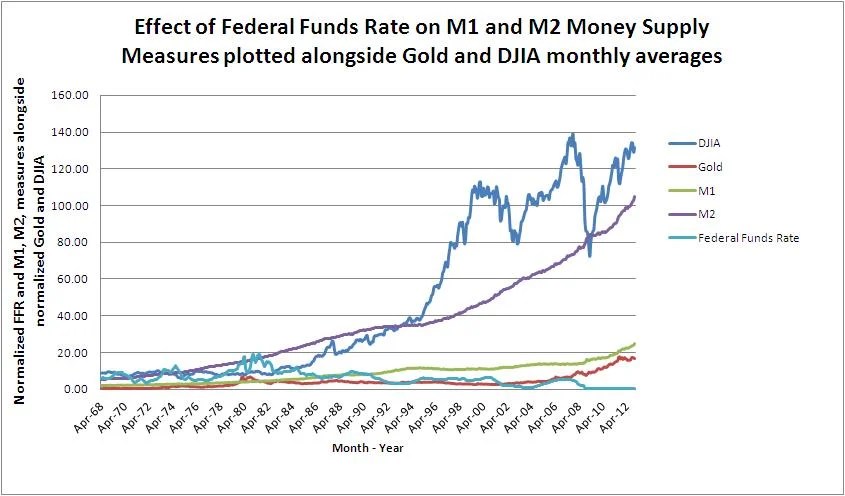

Yellen deflects Hilsenrath from the dot plots and then goes on to target the end of 2016 as the time when rates will likely rise. She also calls out 6.5% as the target for the unemployment rate, and reiterates the eternal 2% target for inflation as triggers for tightening. As you can see below, unemployment clocked in at 6.7%, meaning tightening could be around the corner.

This degree of upside uncertainty, which Yellen interjected as part of her great work at the press conference, managed to spook markets, as, while 2016 may be a long ways off in Yellen’s mind, as it would be when one is waiting to obtain their driver’s license, for those who are writing bonds today based on the Fed’s guidance, 2016 is in many cases a thing of the past, and Yellen’s utterances shattered a countless number of assumptions that the bond market had begun to hold dear.

Conjuring credit out of thin air is risky business as it is, and when those who are primarily responsible for it attempt to explain their actions, things can become incoherent in a hurry.

In the near future, we may hear Yellen uttering Nehemiah’s refrain the next time she is called to the press conference,

“I am doing a great work, so that I can’t come down. Why should the work cease, while I leave it, and come down to you?”

For the last time Yellen came down, fixed income nearly imploded. The risky business of conjuring credit out of thin air is best performed in the dark, if at all.

Stay tuned and Trust Jesus!

Stay Fresh!

Email: davidminteconomics@gmail.com

Key Indicators for March 29, 2014

Copper Price per Lb: $3.02

Oil Price per Barrel: $101.07

Corn Price per Bushel: $4.92

10 Yr US Treasury Bond: 2.71%

Bitcoin price in US: $501.24

FED Target Rate: 0.08%

Gold Price Per Ounce: $1,295

MINT Perceived Target Rate*: 0.25%

Unemployment Rate: 6.7%

Inflation Rate (CPI): 0.1%

Dow Jones Industrial Average: 16,323

M1 Monetary Base: $2,694,800,000,000

M2 Monetary Base: $11,229,900,000,000

You must be logged in to post a comment.