The liquidity drain initiated by the People’s Bank of China has caused a fire sale on financial assets across the globe as Chinese banks scramble to make various margin calls in the face of double-digit overnight rates. Lee Adler, over at the Wall Street Examiner, offers some insight into the big squeeze currently underway:

For the uninitiated, we beg of you to take a step back and to leave, just for a moment, any thought of “efficient market” hypotheses and market fundamentals behind and see the financial world for what it is: A bunch of corporations with large credit card bills to pay and margin calls to meet.

Like anyone who has a large credit card bill to pay or margin call to meet, the ability to meet the obligation is more often than not determined by the willingness of other large corporations in similar situations to lend them money. If they can, great, the credit rolls over. If not, assets must be liquidated so that the debt can be paid.

The flaw in efficient market theory, with regards to financial markets, is that it implies stability when, in fact, most debtors, especially big ones, only liquidate assets as a final option. As such, this type of liquidation often occurs suddenly and with little warning, hence the feeling of panic and cascading financial markets.

At their core, equity markets represent decisions at the margin. They often reflect this type of liquidation in an exaggerated manner. In an odd way, this sort of whiplash seems to be the only way to spur Central bankers into action.

The actions of the PBoC suggest that they have had enough of the easy money policy that has dominated Central Bank actions for the past five years. They have pulled the plug. Does it have anything to do with Mr. Snowden? Who knows, but it is what it is.

As it stands now, the Federal Reserve and Bank of Japan now stand alone on the mountain of insane monetary policy, watching the smoke plumes rise.

Anyone who has perused The Mint no doubt has noticed that we keep a relatively small collection of coins online. This serves a dual purpose. First, it allows us to quickly grab marketing copy should we have a particular coin in stock. Second, it allows us to savor the coin as we attempt to put its dual faces into words. Normally, this can be a tedious and relatively dull process.

1 OZ .999 Fine Silver First Anniversary Mount St. Helens Harry Truman Commemorative Round – 1981

Today was different, as we came across a relatively rare 1 OZ .999 Fine Silver First Anniversary Mount St. Helens Harry Truman Commemorative Round, minted in 1981. For those who are unfamiliar with Harry R. Truman, we offer our marketing copy as a brief descriptor:

On one side of this coin is a bust of Harry R. Truman, the caretaker of the Mount St. Helens Lodge at Spirit Lake who stubbornly refused to leave his home even as the historic eruption was imminent. Truman was 84 when the Mount St. Helens erupted and is presumed to have died along with his 16 cats and 56 others that fateful day on May 18th, 1980. Truman’s bust is surrounded by the inscriptions “Courage,” “Spirit,” “Determination” above and his name, “Harry R. Truman” and the years he was born and died, “1896 – 1980″ below. The letters “KU” appear to the right, their meaning is unknown.

On the other side of this reeded coin is a depiction of Mount St. Helens erupting flanked by the inscriptions “One Troy Ounce” and “.999 Fine Silver,” to indicate its weight and silver content. The top of the coin, just above the smoke plume, is adorned with the inscription “First Anniversary.” Below the mountain are inscribed “1980 – 1981,” and the words “Mount St. Helens.” These beautiful coins are a great way to inspire your friends, loved ones, and co-workers by recalling the finer qualities of a man who became a hero for sticking by his desire to ride out a violent act of nature, come what may.

Mr. Truman, may he rest in peace, in many ways represents the Fed and BoJ today. The other Central Bankers of the world have stepped cautiously back, away from the dreadful inflation for which the eruption of Mount St. Helens will serve as a handy metaphor of today.

1 OZ .999 Fine Silver First Anniversary Mount St. Helens Harry Truman Commemorative Round – 1981

Not Mr. Bernanke and his Japanese counterparts. Both the US Dollar and Yen have been on the mountain longer than many of their counterparts, and their current caretakers are convinced that the bubbling inflation that their policies are stoking will simply blow over as they has in the past.

Are they right? Or is it time to move away a safe distance from the mountain?

A quick peek at the financial markets over the last two days may lead one to think the world is ending. From what we can tell, investors are attempting to front run what they perceive to be an earlier than anticipated FED exit from its unprecedented support of the Bond market to let it fend for itself.

Lest us be clear, the Federal Reserve will not exit when anyone expects it. The mere prospect of it, which began to transmit itself through the markets on Wednesday, caused Treasuries to collapse towards normal and overnight lending in China to seize up while leaving equities and commodities as collateral damage. M1 even managed to collapse again to $2.4 trillion. These are hardly long-term (or short-term, for that matter) Fed goals.

If Fed history is any guide, it shows that the Fed knows absolutely nothing. For example, can you predict what GDP or unemployment will be in one, two, or three years? Neither can the Federal Reserve governors, who are tasked with controlling such matters. The only difference between the man on the street and a Federal Reserve governor with regard to such matters is that the wild guess of the man on the street is more likely to be accurate than that of the Fed governor, but that is a tale better wound by those more qualified to explain such matters, such as Lee Adler at the Wall Street Examiner.

We are gearing up to publish our Treatise on political economy, Why What We use as Money Matters, before we head out on holiday this year. It is more than a treatise, it is our calling (more below).

The current plan is to copy-edit and self publish this important work unless we are successful in landing an interested publisher in the interim. It is urgent that mankind examine what is in their wallet, for it is currently an invisible hand steering mankind towards a myriad of disasters that are either unfolding or about to unfold. These man-made disasters can be undone, if only a few can grasp what we have to share.

Stay tuned for the release and enjoy the brief introduction below!

Introduction: The Calling

Owen Meany had a calling. The hero in John Irving’s 1989 New York Times bestseller A Prayer for Owen Meany which was later loosely adapted to the feature-length film Simon Birch, believed himself to be God’s instrument in an unswerving and often shocking manner. Owen Meany’s calling was as clear to him as it was confusing, for while he could see the end result, he could not foresee nor fully understand the varied circumstances which guided him to his encounter with destiny.

We believe that, like the fictional Owen Meany, every human being that is alive or has ever lived has a calling, something specific that is to be done in this world that only they and they alone can accomplish. The task may be ignored, but it cannot be delegated. It may require the collaboration of many to accomplish, but the burden and drive to complete the task rests with one individual.

If the task does not get done, it does not get done, and the world will be all the worse off for it. On the other hand, if it is accomplished, all the host of heaven will applaud, for every calling that is recognized and pursued is not simply another task to be completed, it is an indispensable stitch in the fabric of what may be if only all of humanity would accept the call to a higher purpose that, far from being reserved for the exceptional, is the birthright of every human.

The following nine volumes are our calling. Taken individually, they are a winding exploration of philosophy, monetary theory, economics, dual entry accounting, climate change, and eschatology. Taken together, they are a treatise on political economy of such gravity and importance that, if fully understood by even one person among a million, will bring the activities of mankind into a perfect balance with nature.

Over the past week the M1 money supply has come roaring back from its relative collapse over the prior two weeks. Today, the measure sits at $2.6 trillion.

M1 consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) traveler’s checks of nonbank issuers; (3) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (4) other checkable deposits (OCDs), consisting of negotiable order of withdrawal (NOW) and automatic transfer service (ATS) accounts at depository institutions, credit union share draft accounts, and demand deposits at thrift institutions. Seasonally adjusted M1 is constructed by summing currency, traveler’s checks, demand deposits, and OCDs, each seasonally adjusted separately.

M2 consists of M1 plus (1) savings deposits (including money market deposit accounts); (2) small-denomination time deposits (time deposits in amounts of less than $100,000), less individual retirement account (IRA) and Keogh balances at depository institutions; and (3) balances in retail money market mutual funds, less IRA and Keogh balances at money market mutual funds. Seasonally adjusted M2 is constructed by summing savings deposits, small-denomination time deposits, and retail money funds, each seasonally adjusted separately, and adding this result to seasonally adjusted M1.

In layman’s terms, the M1 Money supply is what we refer to as “Money on the street,” or cold hard cash. It is the part of the money supply that is otherwise unencumbered or loaned out on float.

The M2 Money supply is perhaps best defined as the Money on the street (M1) plus all of the money that customers think is held at banks but is really loaned out.

In the past, the Federal Reserve also published the M3 (Broad) Money supply measure, which was essentially all of the money that customers had, thought they had, and/or thought that they could receive (via the inclusion of money market funds and repo instruments). It was perhaps the truest measure of the money circulating in an economy in aggregate. In addition to base money, demand deposits, and time deposits, M3 included what the largest treasuries were holding in quasi money instruments . The Federal Reserve stopped publishing the measure on March 23, 2006 as it began to launch into the stratosphere.

While the Broad money supply (M3) may have crossed the line into credit instruments {Editor’s Note: Here at The Mint we recognize all Central Bank notes as credit instruments by definition}, it was an excellent proxy for inflation, for it gave demonstrated the sum total of how many players were participating in the game of monetary musical chairs that the banks and large treasuries play every evening when they settle up.

The M2/M1 Ratio

Today, we submit for your perusal, a graphic of the M2 Money supply divided by the M1 Money supply (the M2/M1 Ratio) by month for the data sets since January 1, 1959, the first year that the data is easily retrievable, through the first week of June.

Historical Ratio of M2 / M1 Money Supply Measures

For purposes of interpretation, the chart shows the degree to which the M1 Money supply is “leveraged” by commercial banks to create what is reported in the M2 figures. Bear in mind this ratio is a function of both bank reserve requirements and consumer behavior. Generally speaking, the M1 and M2 Money supply measures have been increasing over the span of the chart.

The ratio between them, however, has been on a general increase as well, meaning that the M1 measure has been leveraged. This leverage appears to have peaked around 5.4 during the meltdown of late 2008 and early 2009. Ever since then, it has been on a steady decline and currently stands at 4, just a shade above the straight average of 3.7 for the entire data set.

At a glance, it would appear that the economy, in terms of the M2/M1 ratio, is returning to a healthy balance. In practice, this means that the game of musical chairs that occurs at the Fed settlement each night is a bit less stressful for the participants.

Unfortunately, this ratio appears to be historical with little predictive value save that perhaps a ratio of 5/1 being an indication that the monetary base is overextended.

For the moment, with the downward trend in the ratio intact, it appears that the monetary base that the Federal Reserve has gone to great pains to pad via its QE programs, is intact and ready to support an increase in economic activity. Howver, one must keep in the back of their mind that the money supply itself is fragile, and if confidence in the Fed were to evaporate, all bets are off.

Here at The Mint we have been invited to take part in a summer ritual dating back to 1887, one which we have abstained from participating in for one reason or another for twelve years: Softball.

We began what was a reintroduction to the ritual last night in a double header. There was much familiar and generally a good time was had by all. What was unfamiliar was the unexpected mind/body dynamic that took place as we laced up the cleats, grabbed our glove, and pulled our hat down.

As we trotted out to center field, a position chosen entirely at random as time constraints forced our team to tacitly choose positions on the fly, our mind took a trip back some 20 years to our high school baseball days. Unfortunately, our body, which must deal with reality, did not make the trip.

The Georgia Peach in a 1910 photo Courtesy of the George Grantham Bain Collection (Library of Congress)

What followed was a series of misguided exertions and poorly judged balls that passed for softball only by virtue of our dress and physical location. While we avoided striking out, the results were far from optimal. With every successive exertion, our already limited range in the position made famous by Ty Cobb, Mickey Mantle, and Willie Mays, became even more limited while the range perceived by our 17 year old mind grew to that exercised by the Georgia Peach himself.

Towards the end, we found ourselves playing just a shade off the infield and found ourselves in a number awkward instances where we were unnecessarily obligating ourselves to replicate Mays’ famous Catch with quite different results.

However, today is another day and brings another double header with it. How will it turn out? Fortunately, our body is only beginning to seize up and we should avoid the full physical consequences of last nights folly until at least tomorrow.

The M1 money supply is racing upwards once again after a dramatic drop over the past two weeks. Equities, Fixed Income, and Gold are beginning to exhale, which means an inordinate amount of dough is set to run through a supermarket near you.

To make matters worse, or better, depending upon your preference for more Quantitative Easing on the part of the FED, the BLS (sans L) Unemployment rate ticked up to 7.6%, virtually ensuring that the program will remain in place. Despite recent speculation of a taper, QE is the only thing standing between the big banks and insolvency.

The private intelligence firm Stratfor publishes a weekly report on the positioning of US Naval assets using non-classified, open source information available to the public. While this week’s report does not appear to contain any surprises, they can provide valuable insight into the movements of the primary means by which the United States projects its military power across the globe.

The complete report and graphic are republished here with permission of Stratfor:

U.S. Naval Update Map: June 6, 2013

U.S. Naval Update Map: June 6, 2013 is republished with permission of Stratfor

The Naval Update Map shows the approximate current locations of U.S. Carrier Strike Groups and Amphibious Ready Groups, based on available open-source information. No classified or operationally sensitive information is included in this weekly update. CSGs and ARGs are the keys to U.S. dominance of the world’s oceans. A CSG is centered on an aircraft carrier, which projects U.S. naval and air power and supports a Carrier Air Wing, or CVW. The CSG includes significant offensive strike capability. An ARG is centered on three amphibious warfare ships, with a Marine Expeditionary Unit embarked. An MEU is built around a heavily reinforced and mobile battalion of Marines.

Carrier Strike Groups

The USS Dwight D. Eisenhower CSG with CVW 7 embarked is conducting missions supporting Operation Enduring Freedom, maritime security operations and theater security cooperation efforts in the U.S. 5th Fleet AOR.

The USS Nimitz CSG with CVW 11 embarked is conducting maritime security operations and theater security cooperation efforts in the U.S. 7th Fleet AOR.

The USS Carl Vinson is underway in the Pacific Ocean for routine training.

The USS Harry S. Truman CSG with CVW 3 embarked is conducting a sustainment exercise in the Atlantic Ocean in preparation for an upcoming deployment.

Amphibious Ready Groups/Marine Expeditionary Units

The USS Kearsarge ARG with the 26th MEU embarked is underway in the U.S. 5th Fleet AOR supporting maritime security operations and conducting theater security cooperation efforts.

The USS Wasp is underway in the Atlantic Ocean for routine training.

The following is an excerpt from our upcoming ebook release, “To Build up the Land, Thoughts on Mankind’s uneasy intercourse with Nature,” due to hit digital shelves late this week. Enjoy!

To Build up the Land

The Land Needs Rest

There is indeed a perfect balance between the time for building up the land and that for allowing the land to rest. It is commonly known as the Sabbath, it is a pattern of time that has literally been encoded into the creation itself.

The Sabbath is best known, at least in the United States, as part of Jewish religious observances. The base of the observance is taken from two passages in the Torah:

2 On the seventh day God finished his work which he had done; and he rested on the seventh day from all his work which he had done. 3 God blessed the seventh day, and made it holy, because he rested in it from all his work of creation which he had done.

Genesis 2:2-3

12 “Observe the Sabbath day, to keep it holy, as Yahweh your God commanded you. 13 You shall labor six days, and do all your work; 14 but the seventh day is a Sabbath to Yahweh your God, in which you shall not do any work, you, nor your son, nor your daughter, nor your male servant, nor your female servant, nor your ox, nor your donkey, nor any of your livestock, nor your stranger who is within your gates; that your male servant and your female servant may rest as well as you. 15 You shall remember that you were a servant in the land of Egypt, and Yahweh your God brought you out of there by a mighty hand and by an outstretched arm. Therefore Yahweh your God commanded you to keep the Sabbath day.

Deuteronomy 5:12-15

The seven day weekly cycle that is anchored by the Sabbath is so entrenched in the creation that every attempt by man to supersede it, the most notable recent attempts being the French Republican Calendar and the Soviet Calendar. Both were suspended after experiments that lasted roughly twelve years.

While the texts in the Torah, which form part of the Christian Bible, offer clear guidance of the divine to observe not only a seven day week, but a seven day week consisting of six days of work and one day of rest, religious tradition alone cannot account for the origins of the seven day cycle.

Cultures throughout the world have operated on weekly structures consisting of anywhere between three and thirteen days, notable ancient examples are the eight day Roman market calendar and the 13 day Mayan week. Indeed, it appears that even the Jewish Sabbath was not observed by the Jews until they were exiled to Babylonian captivity between 597 and 587 BCE.

Adding to the mystery of the seven day week is that it is they only time construct known to mankind that does not conform to any astrological, lunar, or solar cycle, as days, months, and years are designed to do.

The reason that the seven day weekly cycle, ordained in the Torah, has emerged as the dominant time cycle that is now observed by every large society on the planet, is that seven day cycles are deeply ingrained in both plant and animal life at a cellular level.

Dr. Franz Halberg at the University of Minnesota, is the foremost authority on natural rhythms which is the subject matter of an area of science known as chronobiology. Halberg’s research has shown that all rhythmic functions of the human body are likely to possess an innate seven day frequency.

The divine call for a day of rest every seventh day appears to fit perfectly with an unseen but deeply felt rhythm common to the interplay between all living things down to the most basic cellular level.

While an understanding of the seven day weekly cycle and the need to collectively rest on the seventh day is somewhat easy to grasp based on personal experience for most, what is harder to grasp but equally and perhaps more important with regards to building up the land is the need for the land to rest every seventh year.

In other words, the seemingly arbitrary command to abstain from work on the seventh day not only applies to the cycle of days known as the week, but the need to rest on the seventh year of a cycle after six years of production.

Again, the basis for the resting of the Land on the seventh year by abstaining from all productive agricultural activity can be traced to the Torah:

10 “For six years you shall sow your land, and shall gather in its increase, 11 but the seventh year you shall let it rest and lie fallow, that the poor of your people may eat; and what they leave the animal of the field shall eat. In the same way, you shall deal with your vineyard and with your olive grove.

Exodus 23:10-11

2 “Speak to the children of Israel, and tell them, ‘When you come into the land which I give you, then the land shall keep a Sabbath to Yahweh. 3 You shall sow your field six years, and you shall prune your vineyard six years, and gather in its fruits; 4 but in the seventh year there shall be a Sabbath of solemn rest for the land, a Sabbath to Yahweh. You shall not sow your field or prune your vineyard. 5 What grows of itself in your harvest you shall not reap, and you shall not gather the grapes of your undressed vine. It shall be a year of solemn rest for the land. 6 The Sabbath of the land shall be for food for you; for yourself, for your servant, for your maid, for your hired servant, and for your stranger, who lives as a foreigner with you. 7 For your livestock also, and for the animals that are in your land, shall all its increase be for food.

Leviticus 25:2-7

The command to rest the land every seventh year is often embodied in a practice that is known as crop rotation. Crop rotation is a method of agriculture in which a series of different types of crops are planted in the same area, usually a field, in sequential growing seasons.

The planting of different seeds on the same field each season helps the land to achieve balance because different types of plants require from and provide to the land different types of nutrients, allowing the land to replenish itself. An additional benefit to crop rotation can be found with relation to pests. By constantly changing the types of crops grown in a certain area, the farmer can avoid the possibility that a pest become entrenched in an area, as simply changing crops can deprive certain pests of the means necessary to establish viable habitats over long periods of time for their colonies.

Many crop rotation plans call for a field to lie fallow for a season. While the benefits of allowing the land to rest are numerous, the most common benefit of this practice is that it allows the water table underneath the Land to reestablish itself in anticipation of providing crops for the next six years. Given that water tables are not field specific, but cover large areas encompassing many fields, it is important that the fallow years for fields be coordinated to coincide with each other for the benefits of the Sabbath year to accrue to the Land and, consequently, to the land’s inhabitants.

While it is difficult to comprehend the moral implications of the fact that Margaritaville currently holds the throne as the most lucrative song ever, what is not difficult to comprehend is its allure, a laid back, carefree lifestyle tinged with a hint of regret and melancholy made tolerable by the beach and the “frozen concoction that helps me hold on.”

It is a lifestyle whose allure quickly fades to the harshness of its demands. Beyond the headaches and marked lack of depth in human relations, alcohol sans moderation will inevitably hasten one’s march to the grave. Indeed, despite the headlines received by the AIDS epidemic, warfare, and famine, it is often an addiction to cheap alcohol and that contributes to shortened lifespans in developing nations.

There is no way around it, alcohol is hard on one’s system.

As alcohol is hard on the human system, cheap money is hard on the real economy, and will eventually be purged. At the moment, the M1 money supply is collapsing as the increasing doses of cheap credit have an ever decreasing effect on the real world hangover that awaits at the end of this binge.

Expect the Federal Reserve and the Central Banks of the world to fire up the blenders and roll out the kegs, for a drunk economy is the only one they know.

You can watch Buffet perform his three chord pot of gold here:

How long will the frozen concoction help them hang on? Probably not too much longer.

The following is a guest post on a timely topic by David Bonner, a financial consultant with a passion for helping people find freedom by becoming good financial stewards. Enjoy and stay fresh!

There are many biblical principles when it comes to finance. Perhaps the most often cited is Jesus’s instruction to “Render unto Caesar what is Caesar’s.” Like most of the times that Jesus is quoted in popular culture, this is taken out of context at least as often as not. While I am very much in favor of personal responsibility, good stewardship, and accountability to authority and government, the concept of rendering unto Caesar is not anywhere near so valuable as the biblical principle of Jubilee.

In the book of Leviticus, debts and enslavement are both addressed as coming to an end after fifty years. The Covenant Code, taken from Exodus, includes similar provisions after a period of seven years. This code adds a layer to the idea of rendering unto Caesar in that the debt or the term of slavery – note the biblical application as given to Moses’s audience would have been much more of a household servitude like an indentured servant than our modern interpretation of slavery – should be served out for a reasonable period but not leave people laboring their entire lives under its burden. Unfortunately, apart from bankruptcy, our modern society doesn’t have many allowances for this form of grace. And even bankruptcy does not extend the full protection that many believe it will.

The best time to be responsible with debt management is before taking it on. For this reason, tools like a home loan calculator are invaluable. A mortgage loan calculator or similar tool can help you determine what housing options you can reasonably undertake based on an in-depth understanding of your finances. However, with the soaring costs of education, the massive investment of establishing oneself in almost any career, and the instability of most markets, debt is a reality of modern American life.

The important thing is not to let debt overwhelm you. Part of avoiding this would be to utilize a good debt repayment calculator to determine what money you actually have available to work with. A debt consolidation calculator can help you view all of your debts, credit cards and mortgages, car payments and education loans, together in one focused picture.

This focused picture will enable you to see your finances in terms of available funds rather than seeing your monthly income as being available. A debt elimination calculator will help you select the repayment timeline that works for you, and commit to following through on it. Utilizing debt calculator(s) applications when considering undertaking a big financial step will allow you to make a clear headed and responsible strategy, enabling you to both render unto Caesar and celebrate your own Jubilee before too long.

Dave Bonner runs a small business in the Greater Philadelphia Area, where he lives with his wife and their one-year-old puppy. His consulting work includes applying sound Biblical principles in making economically sound business strategies, a subject on which he has also been privileged to teach. Debt consolidation has become something of a hobby, as he works to assist his friends and family in the pursuit of financial stability and good stewardship.

We were honored yesterday to be mentioned alongside a host of names with more weight and prestige than our own by a writer whom we greatly admire, Jason Hommel, on a list he has compiled of Christian Libertarian resources. We have often referred to Mr. Hommel’s vast trove of research into both the silver market and eschatology (specifically the scriptural and empirical support for a pre-tribulation rapture), which he has published at both the Silver Stock Report and bibleprophesy.org respectively, in our own investigation of these matters. Indeed, Mr. Hommel has performed the world a great service through much of what he shares.

While we do not know him personally, we appear to share similar interests and applaud his bold search for truth and, perhaps more importantly, the tenacity with which he defends it once discovered. Most who have tried find that truth is not often welcomed this side of heaven, at best it is ignored and then attacked as others come to know it. Well done Jason, we cheer you on from our corner of the world and wish you all the best!

The matter gave us pause to think about what it means to be a Christian Libertarian. Indeed, some who may be reading this site on Mr. Hommel’s may wonder where we stand on certain matters.

There two things that we we know. One, that the God of the Bible is the one true God, and that He is our friend. He revealed himself to us and, we believe to all of humanity, through the Messiah, commonly known as Jesus in our experience. In this revelation, he made it clear that we are to Forgive as He has forgiven us, it is his one simple requirement. Sacrifices are meaningless, what He desires is to be close to us. We know that we will live with Him for eternity, no matter what happens here and now.

If this makes us a Christian, so be it.

We also recognize that God has given all of us a free will, which is a logical precondition for His relationship with us. Some use this free will to liberate others, some use it to enslave them.

Yet it is clear that the whole mass of humanity is obligated to respond to the demands of an inherently anarchic world of our own devising because of our willful ignorance and defiance of God. For both those of us who know and love God and those who are either ignorant of or defiant towards Him, our only hope of survival lies in our willingness to peacefully cooperate with one another. This cooperation works best when it is done voluntarily without compulsion.

If this makes us a Libertarian, so be it.

Naturally, there is much more to say on both subjects, and we do pray that you will tune in from time to time. We have attempted to collect our stream of consciousness, for lack of a better term, in a series of ebooks. We are currently working on the last volume of what will be our mini treatise, “To Build up the Land,” which we hope to have on digital shelves by the end of May.

Shifting gears to the Money Supply, the M1 measurement clocked another steep week over week decline, this time on the order of 2.12%. Again, while the week to week shifts in base money are volatile by nature, this now constitutes an 8% + drop.

This is bad news on a number of levels, and the Central Bankers of the world are now moving into overdrive with respect to money creation. Will the succeed in holding off the coming depression?

Thanks again for reading and a special thanks to Mr. Hommel, we consider mention on your site to be a great honor. Be encouraged in your work, for it is extremely important.

Here at The Mint, we have begun to offer a variety of services to fill the needs of our clients as they arise. We began with a humble Virtual CFO offering, an offering that most closely aligns with our skill set. While the offering has met with sporadic success, we have seen a recurrent need amongst those soliciting services, it is a primordial need common to all enterprises: Funding

In response to this emergent need, we are adapting our service offerings to provide marginal companies with the tools and expertise they need both to seek out funding and to concurrently get the company in shape to be able to successfully solicit and deploy said funding.

We generally begin by evaluating their accounting and bookkeeping needs. A brief tour through a company’s financials will reveal much about that company’s state of development and actual prospects. Our bookkeeping and services strive to leverage technology, such as Quickbooks Online (which is emerging as a beautiful platform if one has a relatively fast internet connection and somewhat basic bookkeeping needs, as most startups do), to streamline and automate the bookkeeping function as much as possible. The idea is to pull transactions from the bank and reclassify them.

The process may seem somewhat backwards, especially to the seasoned accountant. Yet, if coupled with strong cash projection techniques, it is hands down the most efficient and cheapest way to process payments and accounting data. Depending upon current processes, we can generally whittle bookkeeping and financial reporting down to 8 hours per month or less per startup client.

Once the bookkeeping house is in order, the hunt for funding can begin in earnest. Currently, we have ongoing funding needs for clients in the following areas:

– Payment processing

– Organic Health and Beauty Products

– Mobile Application development

– Real Estate Investment

– Motion Picture development

– Non-profit Social Services

– Environmentally Conscious Financial Institution

Further, we are in the early stages of establishing investment funds for the following areas:

– The Bolivia Fund: Bolivia is a vastly rich land charged with opportunity. We are fortunate to have great contacts there.

– The Global Venture Fund: This fund is the wild west, it is not for the faint of heart or the shallow of pocket, yet it is a ride that will be the stuff of legend.

All of these ventures and proposed funds are in the concept stage, they are as a baby in the womb, being nurtured, cared for, and protected until their appointed time. Will you be the one to induce labor? If you are an accredited investor in need of an endless fount of creativity, ingenuity, integrity, and business expertise, we have a place for you. To learn more about these opportunities or propose another (ad)venture, please send us an email below.

Adapting to change is the key to survival. While we do not personally ascribe to a macro evolutionary ideology, its survival of the fittest doctrine can be generally applied to companies at the margins. Our services aim to bring these ideas from the margins and give them life, to bridge the gap between fundable projects and funding sources.

While the rally in equities continues relatively unchecked, the measure of the M1 monetary base has taken a marked dive of roughly 6.2% since last week, leaving it at a level not seen since April 15th (see the current M1 measure below).

For the uninitiated, the M1 money supply is what we call cash on the street, coins and bills. In other words, what most people consider spending money.

By nature and by the FED’s own admission, money supply data is highly volatile and subject to revision. Even so, our own observation has been that folks are short on cash. While this brief drop is not likely to signal a change in the trend, it has certainly caused some unexpected hiccups in dollar land.

Perhaps not coincidentally, precious metals have continued their near term price collapse. The price of silver, our preferred investment at The Mint, tanked to nearly $20 overnight Sunday. While the near term price is somewhat irrelevant, it may be indicative of a rush to meet short term debt obligations by holders of precious metals.

Most media reports read much into price movements, as if they mean something about the real economy. Unfortunately, the real economy is nothing more than a yo-yo at the end of a string of debt obligations. Until they wind up the yo-yo and let it be, real economic growth (or contraction of that matter), in terms of debt laden USD land, is nothing more than a myth one reads about in text books and in the main stream financial media.

Eventually, the avalanche of FED funds guaranteed as long as their latest QE pledge is in effect will begin to consistently run into real world asset and commodity prices. It will feel good, but participants are advised to keep their eye on the punch bowl. Once it is removed, it will be best to swim near the edge of the pool.

The vanilla crisis is hitting some chocolate patches, try to avoid them.

Today finds US equity markets up, in fact, they are eclipsing new nominal records. The US economy must see a screaming recovery on the horizon, right?

While the economic recovery, which began in the dark days of 2009 continues to plod along at a predictable pace, there are two factors that are contributing significantly to the determined rise of the equity markets.

First and foremost, strange as it may seem, the US Government is actually paying down debt. A combination of sequester savings, the fiscal cliff with its notable 2% payroll tax increase, and a slew of paybacks on public “investments” made during the financial crisis has the US Treasury somewhat awash in cash, which in turn has caused the supply of US Treasuries on the market to shrink.

In the meantime, the Federal Reserve still has the monetary spigots on full blast and the Primary dealers, who have had their spigots trained on Treasuries, are now directing the overflow into equities, which has caused stocks to rise despite a rise in the US Dollar index (which just passed 83) and the fact that roughly 50% of individual investors are completely out of the stock market. Once Ben Bernanke has his way with the USD and the individual investors get off the fence, this rally will run quite a ways.

The second, and more important factor that is propelling the US Stock indices to record highs, is that it is Tuesday, the day when most people’s 401K contributions and auto investment plans find their way into equities. Zerohedge has provided some interesting analysis as to the effect of Tuesdays on stock indices returns which can be ready here:

This week’s M2 Monetary base shrunk by roughly $100 billion while the M1 Base grew by $80 billion. Generally, this means that more Fed cash has left the hypothetical realm and is out in the world, causing mischief in the form of bidding up prices of everyday goods.

Treasury yields have increased since we last checked in to the tune of 14 basis points. Given that Treasury supply has shrunk over the past month (yes, the US Government actually ran a temporary cash surplus) this decline in yield is not insignificant and may reflect a fundamental change in the dynamic between the Fed and the economy.

Over the past several years, the markets have become accustomed to Quantitative easing taking the form of the Fed printing dollars, lending them to banks at roughly 0.12%, who then soaked up the Treasury supply. The fundamental change that is taking place is that the QE spigot is no longer being soaked up by the Treasury supply, rather, it is flooding the basements of equity markets around the world.

Until now, the commodity markets have remained surprisingly tame in the face of the monetary tsunami that is rushing over the planet. We suspect that the moment may be short lived, and that the time to own anything but dollars is once again at hand.

We return today to complete our series entitled “To Build up the Land.” It is an exploration of the co-dependence of man upon the land, and the land upon man to build it up. While the former statement is obvious, what may be less clear in light of today’s political and environmental climate is the latter.

Does the land really need man to tend to it so that it, too, will prosper? The clear answer is that the land not only needs the activity of man upon it to survive and thrive, but also that of animals. However, the land does not simply require any type of activity, it requires human activity which helps the land to achieve balance.

Today, there are roughly 7.1 billion souls on the planet, more than at any other time in human history. If one watches the numbers roll on the page linked above and then sees that the world’s net population is on track to grow by roughly 80 million souls this year alone, it would appear that this population growth is nothing short of exponential and that the world’s population is on something akin to a warp curve when plotted out graphically.

World Historical Population courtesy of US Census Bureau

However, while 80 million souls per year seems a staggering amount, it is important to note that the actual growth rate, as a percentage of the current population, is on a gentle decline, currently at 1.1%, just half the growth rate experienced in the early 1960’s, which is the most recent peak in the growth rate based on United Nations estimates. The United Nations further anticipates that by 2050, the growth rate will again be halved to just 0.5%, and that the world’s population will stabilize at around 10 billion persons after 2100..

As we have explored earlier, overpopulation is largely a myth constructed by persons who both live in crowded urban areas and assume that current statistical trends will invariably accelerate.

The myth is intensified by the fact that a majority of mankind has chosen to live in urban settings and has left large swaths of land to lie fallow, something that benefits neither man nor the land. According to statistics in the 2013 edition of Demographia’s report on World Urban Areas, roughly three out of every ten, or 28.2% of the world’s population lives in an urban area of over 500,000 total inhabitants with an average density of 14,000 persons per square mile.

The current increase in urban populations and corresponding worldview has left an increasing burden on those who build up the land via agriculture to provide the food necessary for the 7.1 billion souls and counting to survive and be adequately nourished.

If one, for the sake of argument, were to make the broad assumption that those living in urban areas were completely reliant on their rural counterparts for their food supply in an equal proportion, this would mean that the rural population must produce, on average, 139.3% of their annual food consumption. In other words, they must produce enough food for both 100% of their own consumption and an additional 39.3% to be consumed by the otherwise occupied urbanites.

However, this is an overly simplified view of the actual dynamics of food production, for while it is clear that while a small proportion of urbanites may collectively achieve communal or territorial self sufficiency when it comes to food production, it is also clear that 100% of the earth’s rural inhabitants are not dedicated to agricultural.

What, then, is the true ratio? How many persons are spending their lives building up the land?

On average, each American farmer produces enough food to feed 155 people. This is up from roughly 26 people in 1960 and, in terms of statistics, would mean that one person armed with the proper agricultural equipment, technology, and favorable climate patterns, can produce 15,500% of their own caloric requirements.

This staggering advance in American agricultural productivity is largely owed to the extended period of peace which has reigned in America which gave birth to, or at a minimum coincided with, rapid advances in agricultural science and industrial machinery.

It may be said, then, that these advances in agriculture have made possible the urban centric worldview that is widely espoused today. This is not a bad thing, however, and the current awareness of climate change and its potential impact on the increasingly delicate food chain upon which an increasing majority of the world depends is rightly cause for alarm.

Agricultural Alarms

GMOs

While it is staggering that one American farmer can provide nourishment for up to 155 persons, the question that is at the heart of the present debate on the merits of using Genetically Modified Organisms in seeds and the modified seeds’ reliance upon pesticides to ensure adequate crop yields is the following: At what long term cost does this productivity come?

It is an important question, for the long term security of the world’s food supply may hang in the balance.

Genetically Modified Organisms, or GMOs, are a prime example of mankind’s attempt to control nature. It is a form of conservation in that it attempts to conserve the current balance of food production by creating crop yields in excess of that which would occur under normal conditions.

It cannot be argued that GMOs have played a major role in human population growth. However, it is also clear that there are many direct and indirect side effects to exerting this type of control over the food chain which have yet to fully manifest themselves.

First and foremost, the staggering crop yields that the combination of GMO seeds, fertilizer, and pesticides provide come at a high price for the land itself. Rather than achieving a balance with the land, allowing it to produce and rest in natural occurring intervals with intermittent obligatory rests in the form of Sabbath years for agricultural land and herd rotations for pasturelands, mankind’s GMO induced yield highs convert the land into an addict, unable to function without regular shots of fertilizer and irrigation.

Again, fertilization and irrigation are important parts of farming and the building up of agricultural land when done in moderation. However, when these tasks are taken to the extremes under which they are practiced today, they rob both the land and mankind of their most important survival mechanism; self sufficiency.

CAFOs

Another less known but equally widespread practice that may ultimately threaten the food supply is the increased reliance upon Confined Animal Feeding Operations, or CAFOs. The proliferation of CAFOs, which are facilities where animals are raised in relatively cramped quarters and fed things that are not part of their natural diet (the equivalent of fertilizer in the GMO example above) and injected with antibiotics (the equivalent of pesticides in the above example) poses a twofold threat to the environment.

First, it produces animal based foodstuffs that have been proven to be harmful to humans over time. Second, and perhaps more importantly for reasons that are obvious, it limits the animals’ natural and mutually beneficial interaction with the land which robs the land of an important means of natural fertilization and rejuvenation, urine and manure.

After a personal epiphany regarding the detriments of setting apart land for conservation, a practice that is widely thought to be beneficial, Ecologist Allan Savory has made it his life’s work to reverse what he now sees as a dangerous policy of conservation.

For over a century, well meaning ecologists like Mr. Savory have labored under the belief that desertification, the fate that awaits the land when mankind and animals cease or severely limit their intercourse with it, was the direct result of large herds of animals grazing upon it. The initial conclusion of attributing desertification to large scale animal grazing is a logical one. After all, if one has seen the relative devastation that large herds leave in their wake, one can only conclude that the animals alone are responsible for desertification, as they leave the land barren and trampled.

Yet Savory holds out that this first analysis is incomplete. In fact, it is necessary for animals to consume, trample on, and leave their excretions on the land so that it may be left in peace to rejuvenate itself with the necessary fertilizer and just the amount of greenery necessary to thrive.

Part of the logic of Mr. Savory’s approach is that if the animals are left to graze freely, they will leave the land for greener pastures, as it were, once they have eaten the top layers of grass and shrubbery, the equivalent to pruning a plant. Furthermore, the animals will quickly tire, as anyone would, of tromping through their own excrements in search of food, leaving the land both pruned and fertilized. The land will then rejuvenate itself in time for the next grazing cycle.

While it has remained on the fringe of land management, Mr. Savory’s work has received the endorsement of royalty. At the 2012 World Conservation Congress, none other than the Prince of Wales gave this endorsement of Savory’s methods:

“I have been particularly fascinated, for example, by the work of a remarkable man called Allan Savory, in Zimbabwe and other semiarid areas, who has argued for years against the prevailing expert view that it is the simple numbers of cattle that drive overgrazing and cause fertile land to become desert. On the contrary, as he has since shown so graphically, the land needs the presence of feeding animals and their droppings for the cycle to be complete, so that soils and grassland areas stay productive. Such that, if you take grazers off the land and lock them away in vast feedlots, the land dies.” {via wikipedia.org}

While GMOs and CAFOs may appear to be nothing short of modern miracles with respect to food supplies, they are a result of man attempting to control the land as opposed to working with the land for mutual benefit. Left to its own devices, mankind will destroy the land to the extent that it wishes to unilaterally exert its will upon it. What is needed, then, is an acute awareness that to destroy the land through an exertion of unnatural control over it, is to destroy ourselves.

Conservation dooms the land to desertification

It is clear that the land, mankind, and animals live together in a delicate balance. Maintenance of this balance requires both constant interaction between mankind and nature and a measure of restraint, a general recognition that nature cannot be controlled in a healthy manner.

The opposite of the action of building up the land is a term that implies something that could not be farther from the truth: Conservation.

The term conservation implies the maintenance and upkeep of something. In terms of land management, it may be mistaken for actions taken or not taken to build up the land. However, in practice, conservation has come to embody a form of forced abstinence on the part of man with regards to the land.

There is much debate and scientific evidence which points to the activities of mankind being the ultimate cause of climate change and desertification. These findings are true to the extent that mankind’s activities are not aimed at building up the land. However, the only thing worse than mankind working to throw nature further out of balance by chasing a misplaced monetary premium is for mankind to abstain from interacting with the land altogether in a vain hope that the land would be better of without us.

The land needs mankind, and mankind needs the land. Both the land and mankind need animals to freely roam over the land rather than suffer in the constraints of a CAFO, the equivalent of prison in the animal world. All efforts to halt this natural interaction are an unwitting step towards squandering what arable land remains on the planet.

In today’s fast changing world, it is increasingly important to maintain one’s competitive edge. Technological breakthroughs are either eliminating jobs or shifting work around at a breakneck pace and if one is to survive and thrive under such conditions, complacency is not an option.

The following are three great articles which are worth a read by anyone working to gain, maintain, or increase their competitive edge.

First, Keld Jensen over at Forbes lo

What is Money? By David Mint

oks at what it takes to succeed, and it may not be what you think. We were once told that a good heart would take us further than good grades. In our experience, this has proven true. Jensen appears to agree in this great read:

Next, Geoffrey James over at Inc.com shares the core beliefs of great bosses. Again, great stuff that we have observed as well. Especially the first one he lists, “Business is an ecosystem, not a battlefield.” We are truly all in this together, and great managers and leaders recognize this as a basic truth:

Rounding out the trio is a piece on productivity by Ilya Pozin again at Inc.com. Timely advice in a world were the need to communicate is trumping the need to produce:

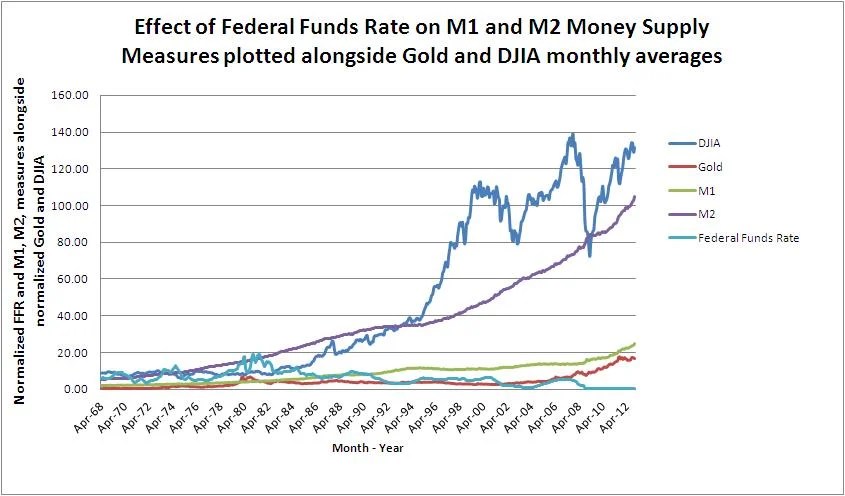

The Dow has briefly touched the 15,000 mark once again and frankly, from a money supply standpoint, it may just be getting started. Ditto for the S&P 500, which is cruising past 1,600 and shows few signs of looking back.

The stock market is front running something. Conventional wisdom, that of seven years ago, would say that it is front running the economy, that a brighter future is on the horizon.

Here at The Mint, we see the stock market as an indicator of the bloat in the money supply and the default primary beneficiary of those who are unloading the monetary premium embedded in the US dollar.

From the dawn of time, up until 1994, the M2 money supply ran ahead of the stock market. Logically, money needed to be created before it could be invested. Then, in 1995, the Glass-Steagall act, which had created a chasm between the commercial and investment flavors of banks since 1933, was effectively repealed as Citicorp and Travelers merged, forcing (or anticipating) the effective repeal of 28 firewalls that Glass-Steagal had set up between the banking sectors.

Graph of normalized DJIA and Gold assets classes vs. M1, M2, and Federal Funds Rate measures

This repeal allowed commercial banks to fund purchases of “Section 20” affiliates, effectively unleashing the credit of the Commercial banking sector into the stock market, and stock indices have front run the M2 money supply ever since (with one notable exception at the height of the 2008 crisis right before the FED threw caution to the wind regarding monetary policy).

The FED will not make the same mistake again. They have embedded expectations that they are willing and able to print money in quantities necessary to avoid another wholesale collapse in the nominal price of financial assets, what we call the chocolate disaster.

However, the FED cannot avoid a collapse in the relative value of financial assets, which is currently underway. While the Dow may be headed to 17,000 before its next scheduled breakdown, the wise among us (that’s you and I, fellow taxpayer), must move our gaze to the diminishing relative value of those 17,000 Dow points.

Take the example of gold. Despite its recent collapse in price, gold, which may have yet another leg down, has shown itself to be incredibly resilient in the face of insurmountable odds, for the same credit mechanism that is used to shamelessly juice the stock market is also used to shamelessly short precious metals.

What is surprising, then, should not be that gold has collapsed some $350 in recent months, but that it has bounced back at all against a financial enemy with an unlimited supply of ammunition.

The physical supply of gold is another story. As anyone who has attempted to source gold or silver at these rock bottom prices can attest, it has been difficult to say the least, and it will be mid summer before supplies recover from the recent price shock.

Another non productive asset that is gaining on the Dow in relative terms is the Bitcoin. While the digital currency continues to be too volatile to trade, it is still attractive anywhere under $80. While not the panacea that many believe it to be, the Bitcoin fulfills a human need that will not soon go away.

Finally, corn, which took a similar early April bath along with a number of commodities, is raging back as well.

It will be an interesting summer indeed as the vanilla disaster continues to pile up. Soon, owning real assets will be not simply a luxury, but a necessity, as gains in the stock indices are dwarfed by real inflationary pressures.

Today at The Mint we are launching The Mint Money Supply Digest. Longsuffering readers of The Mint will recall that we launched a now defunct service known as the “72 Hour Call” which was an attempt to predict the future direction of a specific trade three days out. After roughly 63 attempts, of which we were batting .524 (correct 52.4% of the time) we decided that the short term call was a fool’s game best left to high frequency traders and those with insider information.

However, the 72 Hour Call exercise was not in vain, rather, what it revealed was that while our Key Indicators (listed below), when taken together, revealed no reliable and/or actionable data with regards to short term trades. Over time, however, the Key Indicators have proven extremely helpful in projecting longer term trends which tend to underpin the S&P 500 in particular and US equity indices in general.

Before we go further, we must give credit to both Lee Adler at the Wall Street Examiner and Greg Guenther of the Daily Reckoning’s Rude Awakening for their brilliant coverage of the frequent gyrations in the financial markets. If you need information which is actionable on a shorter time horizon, we highly recommend following their insights.

The intent of The Mint Money Supply Digest is to provide insight via the observation of changes in the trend of our Key Indicators as to the direction of one simple yet critically important trend.

The simple trend is that of the money supply in terms of US dollars. The goal of the monetary stimulus every central bank on the planet has undertaken to some degree or another over the past three to four years has been to simply increase the money supply and hope for the best.

Graph of normalized DJIA and Gold assets classes vs. M1, M2, and Federal Funds Rate measures

The strategy is a recipe for disaster, as we have explored in depth both here at The Mint and in our eBook series “Why what we use as Money Matters.” The goal of The Mint Money Supply Digest is to keep our readers informed as to the trend of the Money Supply in terms of US dollars in an effort to keep you ahead of the curve when the disasters (for there will be a series of them) occur.

The disasters will come in one of two flavors. The first flavor, which we will call vanilla for the moment, takes the form of the increases in the money supply begin to take hold to the point where inflationary expectations by a majority of the actors in the world economy who use dollars or dollar proxies (currencies and debt instruments which are pegged, directly or indirectly, to the US dollar) in trade become embedded to the point where inflation in consumer prices sparks a level of demand in consumer goods which quickly outstrips supplies of such goods. The vanilla disaster is a mouthful, and it is where the trend is gently heading today.

The second flavor, the disaster which is unlikely in the short term save the appearance of black swan type events, we will call the chocolate variety. The chocolate variety of disaster is simple, it takes the form of an unmitigated collapse in the money supply similar to what the world experienced in 2007 (which most people realized was occurring in 2008). Were this to occur, it is time to get all chips off of the table. Fortunately, our Key Indicators should give us roughly three to four years of advance warning of a full blow chocolate disaster taking place (barring the unpredictable, or black swan event, as it were).

As you can see, while the chocolate disaster is to be feared above all, it will be easier to prepare for given the lead time in the data. The vanilla disaster, which is currently underway to some extent, will be somewhat more difficult to pinpoint in terms of timing but will likely have a lead time of roughly two to three months in which to take action.

Our bias, then, at the outset of The Mint Money Supply Digest, is to be on the lookout for the vanilla disaster while gauging, via the trends in our Key Indicators, just how much chocolate is mixed into the swirl which is the combined disaster that is slowly unfolding in US dollar land.

As a logical offshoot of our analysis, we keep an eye on something we call the “Monetary Premium,” which is our term for what most people simply refer to as money. In our worldview, money does not exist in the tangible way that most people assume it does. Rather, the concept of money comes into being when people begin to attach the attributes of money to something which gives that something (usually one of our Key Indicators) a premium above and beyond what normal market conditions and that special “something’s” physical or ethereal composition might otherwise dictate.

This increase in relative value of that special “something” is what we refer to as the Monetary Premium, and it is important, for a big part of making money is accurately identifying not where the monetary premium is, such as the US dollar, but in where it is gravitating towards, such as gold, Bitcoins, or sea shells.

With the preamble out of the way, we hope to keep the Digests as simple and sweet as a cone on a hot summer’s day.

The Mint Money Supply Digest for May 3, 2013

Today the swirl of disasters continues to tend towards the vanilla variety. Jobless claims continued their positive trend and the unemployment rate reported by the BLS came down a notch to 7.5%. This is good news and bad news. Good news in that more people have jobs, and bad news in that every tick down in Unemployment moves the world closer to the day where the Federal Reserve is likely to turn the switch on their monetary Mega maid, their Quantitative easing programs, from suck to blow. That day is still far off, however.

Today’s jobs report, coupled with the ECB’s dovish meeting announcements yesterday (they are throwing in the towel, albeit in slow motion, on austerity) and the BOJ’s Turbo Kids monetary strategy for an aging population are all buoying the money supply to counteract the unmitigated, innavigable disaster that is the world economy. An economy that is desperately trying to reset itself without the benefit of knowing who is really solvent.

You must be logged in to post a comment.